Finding our niche in a crowded digital market

The Canadian digital mortgage space is crowded, so I analyzed the application flows of 4 major companies: nesto, True North Mortgage, Nuborrow, and Rate.ca. My goal was to identify best practices, pain points and opportunities for 360Lending.

Competitors like nesto offer a 100% digital, self directed product. This is fast and efficient for tech-savvy users but can be cold and intimidating for those with complex financial situations.

True North and NuBorrow use digital forms as a more efficient "front-door" to a traditional brokerage service. The experience is better than a simple form but still primarily a tool for lead capture.

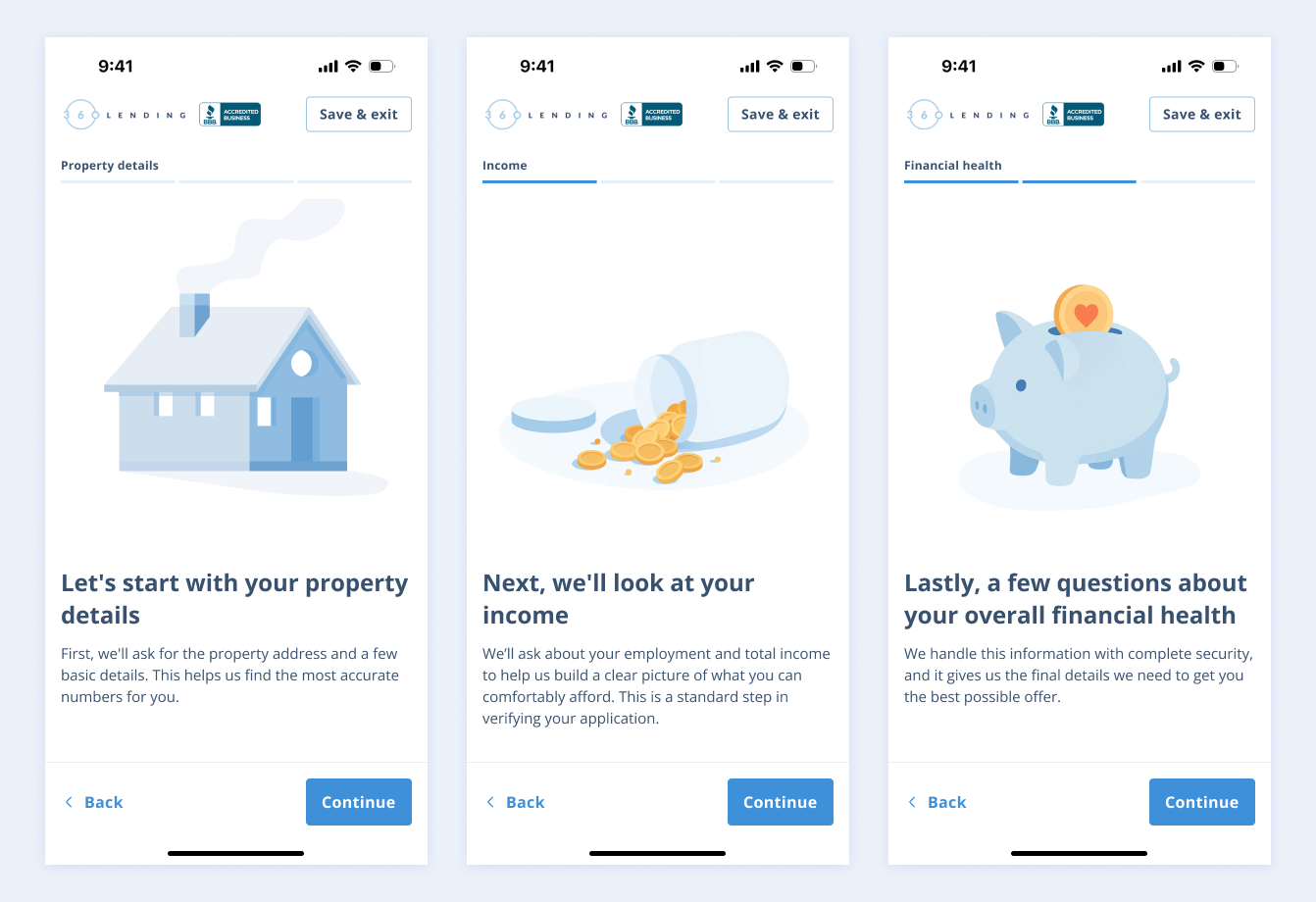

This research made me realize that we needed to design a "smart" application, not just a "fast" one. It needed to ask the right questions at the right time, so that by the time the user finished, they felt understood and the broker received a highly qualified, high context lead.